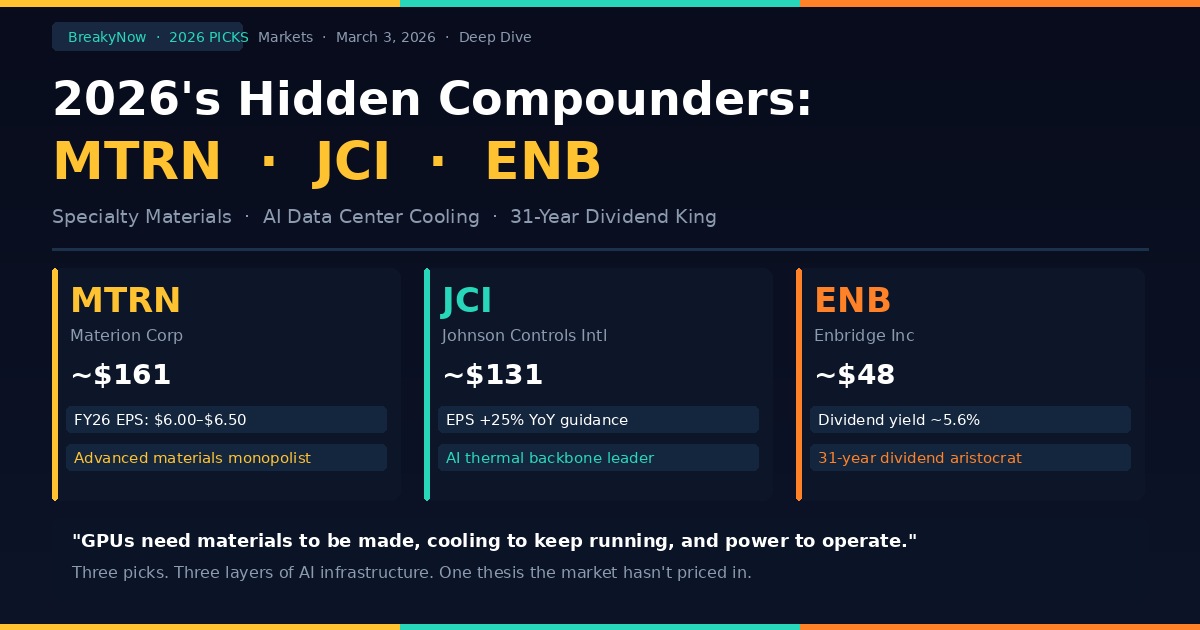

2026's Hidden Compounders: MTRN, JCI, and ENB Are Quietly Building the Infrastructure AI Can't Run Without

A specialty materials monopolist. The thermal backbone of every AI data center. A 31-year dividend growth king with a $39 billion backlog. Three stocks Wall Street hasn't fully discovered — and one shared thesis tying them all together.

Wall Street's AI investment narrative has a recurring cast of characters. Nvidia. Microsoft. Amazon. Palantir. The names rotate but the logic stays the same — bet on the most visible beneficiary of the largest technology transition in a generation. That strategy has worked. It has also left an entire layer of the AI infrastructure buildout almost entirely unappreciated. Building a hyperscale AI data center requires more than GPUs. It requires the specialty alloys and precision materials that semiconductor manufacturing depends on. It requires industrial-grade chiller systems capable of removing megawatts of heat generated by those GPUs continuously and reliably. And it requires natural gas pipelines and energy infrastructure to power the facilities that house them. In 2026, BreakyNow's three highest-conviction underfollowed positions are the companies supplying exactly those things: Materion Corporation (MTRN), Johnson Controls International (JCI), and Enbridge Inc. (ENB). None of them are household names in the AI conversation. All three of them are indispensable to it.

① Materion Corporation (MTRN) — The Quiet Materials Monopolist Behind Every Advanced Chip

What Materion Actually Does

Materion Corporation (NYSE: MTRN), headquartered in Mayfield Heights, Ohio, is a global supplier of advanced engineered materials that most investors have never heard of — and that virtually no technology company can do without. Founded in 1931, Materion designs and manufactures high-performance specialty alloys, precision thin-film deposition materials, optical coatings, beryllium composites, and electronic materials that serve as critical inputs across semiconductor manufacturing, aerospace and defense, medical imaging, and industrial applications. The company's products are not consumer-facing. They are embedded in the F-35's airframe, in the ASML lithography machines that print the world's most advanced chips, in the optical filters of medical CT scanners, and in the precision interconnects of next-generation AI processors. This invisibility is precisely what makes Materion so strategically interesting: the company occupies a position of quiet structural necessity across multiple technology sectors simultaneously, with limited direct competitors at the material science level it operates.

Materion's business operates across three segments. Performance Alloys & Composites supplies beryllium, copper, and nickel-based specialty alloys to aerospace, defense, semiconductor capital equipment, and energy customers. Advanced Materials produces precision sputtering targets, optical coatings, and specialty thin-film materials that are direct inputs into semiconductor fabrication processes. Precision Clad & Coatings manufactures composite clad materials and precision filters for aerospace and medical applications. In a recent strategic expansion, Materion completed the acquisition of tantalum manufacturing assets in South Korea — a direct move to deepen its support for Tier 1 semiconductor customers and extend its global manufacturing footprint precisely where advanced packaging demand is accelerating.

Q4 2025 Results: A Quiet Turning Point

Materion's fourth quarter 2025 results appeared modest on the surface but revealed meaningful inflection beneath. Q4 2025 revenue reached $489.75 million, beating analyst estimates of $448.78 million by 9.1% and growing 12.1% year-over-year — the largest revenue beat in recent memory. Adjusted EPS came in at $1.53, modestly above the $1.51 consensus. Net income turned positive versus a loss in the same quarter a year earlier, with management describing the quarter as a "return to profitability." The Electronic Materials segment led growth, a direct reflection of the accelerating AI chip manufacturing cycle driving demand for Materion's sputtering targets and precision deposition materials. The company also disclosed a $65 million customer investment to support U.S. defense initiatives — a multi-year industrial commitment that underpins durable high-value revenue streams in the defense vertical.

FY2026 Guidance: EPS $6.00–$6.50, Earnings Inflection Confirmed

Materion issued FY2026 EPS guidance of $6.00 to $6.50, set on top of a significantly improved 2025 profit base. KeyCorp analyst Philip Gibbs lifted his FY2026 EPS estimate to $6.50 and established a FY2027 EPS forecast of $7.65, maintaining an Overweight rating with a $170 price target. Simply Wall St's fundamental model pegs fair value at $178.33, implying approximately 15% upside from current levels near $161. The company's long-term narrative projects $2.1 billion in revenue and $355 million in earnings by 2028, requiring roughly 7.2% annual revenue growth — a trajectory that analysts view as achievable given the structural tailwinds in semiconductor and defense end markets.

The Core Investment Thesis: Advanced Packaging and the "Copper Wall"

The single most important driver of Materion's 2026 growth story is the semiconductor industry's accelerating transition to advanced packaging architectures. As AI chips scale beyond what traditional planar designs can achieve, the industry has migrated to chiplet-based designs — multiple dies co-packaged together in configurations like HBM memory stacks and multi-chip modules. These architectures impose unprecedented requirements on the materials that connect chips to substrates and substrates to circuit boards. Traditional copper interconnects are hitting physical limits on signal integrity, thermal dissipation, and form factor. Materion's beryllium-copper alloys, specialty sputtering targets, and precision clad materials are among the leading solutions being adopted as the industry moves beyond copper's ceiling. The South Korea tantalum acquisition reinforces this positioning directly — tantalum-based materials are critical inputs in advanced capacitors and barrier layers used in leading-edge semiconductor processes at TSMC, Samsung Foundry, and Intel Foundry. On the defense side, the F-35, B-21, and next-generation aerospace platforms provide multi-year revenue visibility in beryllium composites that is independent of the semiconductor cycle.

Risks: Cyclicality and Customer Concentration

Materion's primary risks are well-understood. Customer concentration remains the most immediate concern — a small number of high-volatility end markets generate a disproportionate share of revenue, and semiconductor downturns (as seen in 2023–2024) create direct headwinds to order flow. China-related revenue exposure and export control regulatory risk require ongoing monitoring as the geopolitical environment around semiconductor supply chains continues to evolve. Thin net margins during down cycles mean that operating leverage works in both directions — the same structural characteristics that drive earnings recovery during upturns can amplify losses during contractions. Investors should treat Materion's earnings trajectory as linked to the semiconductor capex cycle, with defense acting as a partial but meaningful buffer.

MTRN Scorecard

| Metric | Data |

|---|---|

| Current Price | ~$161 (NYSE) |

| 52-Week Range | $69.10 – $151 |

| FY2026 EPS Guidance | $6.00 – $6.50 |

| KeyCorp Price Target | $170 (Overweight) |

| SWS Fair Value Estimate | $178.33 (~15% upside) |

| FY2027 EPS Forecast | $7.65 (KeyCorp) |

| Q4 Revenue Growth | +12.1% YoY, beat by 9.1% |

| Core Theme | Advanced packaging materials + defense |

② Johnson Controls International (JCI) — The Thermal Backbone of the AI Era

What Johnson Controls Actually Does

Johnson Controls International (NYSE: JCI), headquartered in Cork, Ireland, is the world's leading provider of building products and services — HVAC systems, industrial chillers, building automation platforms, fire detection and suppression systems, and integrated security infrastructure. Its brands include YORK (chillers), Metasys (building management), and OpenBlue (digital services platform). Revenue is generated through hardware and equipment sales, long-term installation and maintenance service contracts, and recurring digital software subscriptions — a structure that provides meaningful recurring cash flow and high visibility into future earnings. In April 2025, JCI completed a reorganization into three regional operating hubs — Americas, EMEA, and APAC — and divested its residential HVAC business to Bosch, using the proceeds to fund an aggressive share repurchase program and redeploy focus toward its highest-growth markets: AI data centers, life sciences, and mission-critical cooling infrastructure.

Q1 FY2026 Results: Record Orders, 40% EPS Growth

Johnson Controls' fiscal Q1 2026 results, reported February 4, 2026, were among the strongest in the company's recent history. Revenue reached $5.80 billion, up 6.8% year-over-year and above the $5.64 billion consensus. Adjusted EPS came in at $0.89, beating the $0.84 consensus by 6% and surging 39% above the prior year's $0.64. Net margin reached 13.95% and return on equity 15.35%. Adjusted EBIT margin expanded 190 basis points to 12.4%, driven by higher service mix and productivity initiatives. Most significantly, the order backlog grew 20% to a record $18 billion — the strongest forward revenue indicator in the company's history. Regional order growth was led by the Americas at +56%, with EMEA at +8% and APAC at +10%, with Americas growth explicitly driven by hyperscale data center construction projects. CEO Joakim Weidemanis described the quarter as delivering "record orders," underscoring the strength in mission-critical markets.

FY2026 Full-Year Guidance Raised: ~$4.70 EPS, ~25% Growth

Following the Q1 beat, Johnson Controls raised its full-year FY2026 adjusted EPS guidance to approximately $4.70. CFO Marc Vandiepenbeeck confirmed this represents "roughly 25% growth." Q2 2026 EPS guidance of $1.11 exceeded the $1.05 consensus. Full-year organic revenue growth is guided in the mid-single-digit range, with approximately 50% operating leverage and roughly 100% free cash flow conversion expected for the year. Revenue is projected to reach approximately $25.1 billion in FY2026, growing to $32.6 billion by FY2030 — driven by electrification initiatives, energy efficiency mandates, and AI-driven data center infrastructure demand.

The Core Investment Thesis: Every GPU Cluster Needs a Chiller

The most important insight behind the JCI investment thesis is straightforward: an AI data center that cannot remove heat cannot operate. A single Nvidia H100 GPU dissipates up to 700 watts. A hyperscale AI cluster housing hundreds of thousands of GPUs generates thermal loads that no existing building cooling system was originally designed to handle. The AI data center construction boom has created a structural, multi-year demand surge for mission-critical industrial chiller systems — and Johnson Controls is the company that builds them. JCI is working directly with Nvidia to apply its thermal management and controls expertise to next-generation AI computing environments. The company published a comprehensive reference guide mapping the full thermal chain for AI factory-scale deployments, positioning itself not merely as an equipment supplier but as the architect of the thermal backbone for the next generation of AI infrastructure.

The new product lineup makes this positioning concrete. The YORK YDAM air-cooled magnetic bearing centrifugal chiller delivers up to 3.5 megawatts of cooling per unit at 20% higher capacity density than prior generation systems, designed specifically for high-density multistory AI data centers. The YKHT chiller supports waterless heat reduction — eliminating up to 9 million gallons of cooling tower water annually per deployment. The newly launched Smart Ready Chiller provides 10 times the operational insights of conventional remote-connected chillers, enabling proactive service relationships and reducing unplanned downtime. These products represent a fundamental shift in JCI's business model: from commodity HVAC equipment supplier to mission-critical AI infrastructure partner with long-duration digital service revenue attached. The pending acquisition of Alloy Enterprises is expected to further enhance thermal management efficiency in data center environments.

Valuation: Still Reasonable Despite a Strong Run

Despite a 58% total shareholder return over the past year and a 25% single-month surge following Q1 results, JCI's valuation remains constructive relative to its growth profile. The stock trades at a forward P/E of approximately 21.9x — below the S&P 500's 26.2x — despite guiding to 25% EPS growth. The TIKR valuation model estimates a target price of $166, implying approximately 15% additional upside even after the recent surge. With a record $18 billion backlog already secured and mid-single-digit organic revenue growth expected, the market appears to be pricing in execution risk rather than acknowledging the structural earnings acceleration underway. Most sell-side analysts carry Buy or equivalent ratings with a consensus 12-month price target around $122–$130.

Risks: Execution Complexity and Multiple Sensitivity

JCI's primary risk is operational execution. The company is simultaneously rolling out a Lean operating system across thousands of employees, expanding a new product portfolio, navigating a major organizational restructuring, and scaling its AI data center business — all at once. A stumble in any one of these initiatives could impair short-term results and compress the multiple. The stock has also already absorbed a great deal of good news: a 58% one-year return means elevated expectations are embedded in the share price, and any slowdown in backlog conversion or margin expansion could trigger outsized selling. Debt remains on the higher side and warrants monitoring, though management's 100% free cash flow conversion guidance implies sufficient capacity to service obligations while funding growth.

JCI Scorecard

| Metric | Data |

|---|---|

| Current Price | ~$131 (NYSE) |

| Market Cap | ~$80.5 billion |

| FY2026 EPS Guidance | ~$4.70 (+25% YoY) |

| Record Backlog (Q1) | $18 billion (+20% YoY) |

| Americas Order Growth | +56% YoY |

| Forward P/E | 21.9× (below S&P 500) |

| TIKR Price Target | $166 (~15% upside) |

| Key Partnership | NVIDIA (AI data center thermal) |

③ Enbridge Inc. (ENB) — The Dividend Aristocrat Hiding Inside the AI Power Trade

What Enbridge Actually Does

Enbridge Inc. (TSX/NYSE: ENB), headquartered in Calgary, Alberta, is the largest energy infrastructure company in North America. It operates across four business segments: Liquids Pipelines, Gas Transmission & Storage, Gas Distribution & Storage (utilities), and Renewable Power. Enbridge's network transports approximately 30% of North America's crude oil production and roughly 20% of total North American natural gas consumption. The critical distinction in Enbridge's business model is that the company is not an energy producer — it is an energy transporter. Revenue is generated through long-term, take-or-pay capacity contracts that charge tolls based on volume throughput regardless of commodity prices. This structure gives Enbridge cash flow predictability that resembles a regulated utility or an infrastructure REIT far more than a traditional energy company. In 2024, Enbridge completed the acquisition of three major U.S. gas utility companies — beginning to flow through fully into 2025–2026 results — dramatically expanding its regulated earnings base.

FY2025 Results: Record EBITDA, 31st Consecutive Dividend Increase

Enbridge's full-year 2025 results, reported February 13, 2026, delivered full-year GAAP net earnings attributable to common shareholders of $7.1 billion (C$3.23 per share), up 39% year-over-year. Adjusted EBITDA reached C$20.0 billion, growing 7% from C$18.6 billion in 2024. Adjusted EPS increased 8% to C$3.02 per share. The Board of Directors declared the 31st consecutive annual dividend increase, raising the quarterly dividend 3% to C$0.97 per share (C$3.88 annualized), effective March 1, 2026. On the NYSE, the annualized dividend translates to approximately US$2.69 per share, implying a forward yield of approximately 5.5%–5.7% at current prices near US$48. During 2025, Enbridge placed C$5 billion of organic growth capital into service and sanctioned C$14 billion in new growth projects — the largest single-year project sanctioning in the company's history.

FY2026 Guidance: EBITDA C$20.2B–$20.8B, ~$8B of New Projects Entering Service

Enbridge's 2026 financial guidance targets adjusted EBITDA of C$20.2 billion to C$20.8 billion and distributable cash flow (DCF) per share of C$5.70 to C$6.10, representing approximately 4% growth from the 2025 guidance midpoint. Approximately C$8 billion of new projects are scheduled to enter service across all four business franchises in 2026, all underpinned by low-risk commercial frameworks. The company's secured growth backlog now totals C$39 billion — a 35% increase since March 2025 — providing extraordinary visibility into future earnings. Beyond 2026, Enbridge reaffirmed approximately 5% annual growth in adjusted EBITDA, EPS, and DCF per share. The 2023–2026 compound annual growth rate outlook stands at 7–9% for EBITDA and 4–6% for EPS.

The Core Investment Thesis: AI Electricity Demand Flows Through Enbridge's Pipes

The most underappreciated dimension of the Enbridge investment thesis in 2026 is its direct linkage to AI power demand. AI data centers are consuming electricity at a rate that existing power grids were not designed to accommodate. Solar and wind power alone cannot provide the 24/7 firm power that hyperscale computing facilities require. Gas-fired generation is the only currently available technology capable of bridging the gap at scale — and gas-fired power plants require natural gas pipelines. Enbridge owns a disproportionately large share of those pipelines. The Gas Transmission team is actively tracking more than 60 potential data center or power-related projects that could substantially increase natural gas demand over the coming decade, representing more than C$4 billion in potential investment by 2030. A specific example: the Cowboy Phase 1 project — a 365 MW solar facility with 135 MW BESS — was sanctioned under long-term agreements to support a global technology company's operations in Cheyenne, Wyoming.

The 2025 project sanctioning list illustrates the breadth of this positioning. The Eiger Express Pipeline was upsized from 2.5 Bcf/d to 3.7 Bcf/d. The Bay Runner extension to the Whistler Pipeline was sanctioned. The Mainline Optimization Phase 1 adds 150,000 barrels per day of capacity to the cross-Canada Mainline and 100,000 bpd to Flanagan South, all contracted under long-term take-or-pay agreements. On the renewables side, a 600 MW Clear Fork solar project for Meta began construction. Together, these projects illustrate a company that is simultaneously winning across conventional energy, LNG growth, and AI-adjacent power infrastructure — a portfolio with genuine diversification across the energy transition.

The Dividend Aristocrat Math: ~5.6% Yield Plus Capital Appreciation

What makes Enbridge unusual in the current market environment is the combination it offers. A NYSE dividend yield of approximately 5.5%–5.7% — in an environment where investment-grade bonds yield 5% — already justifies ownership on income grounds alone. But Enbridge adds to that yield a visible capital appreciation pathway. Citi recently updated its price target to US$77, representing significant upside from current ~$48 levels. TD Cowen remains constructive, aligned closely on DCF metrics. MarketBeat's TSX average price target of C$70.58 implies approximately 6% capital appreciation on top of the mid-5% dividend yield. Add the two together and the total return picture becomes compelling. Enbridge plans to distribute C$40–$45 billion in dividends over the next five years, entirely supported by regulated contracted cash flows. The dividend payout ratio remains within management's target range of 60–70% of DCF, with no common equity issuance planned for 2026.

Risks: Line 5 Regulatory Overhang and Interest Rate Sensitivity

Enbridge's most significant near-term risk remains the Line 5 pipeline regulatory situation. While the U.S. Army Corps of Engineers issued a key reroute permit in October 2025 — a major positive milestone after years of legal challenges — Michigan state-level litigation over the Great Lakes Tunnel at the Straits of Mackinac continues. An adverse outcome would meaningfully impair cash flows from the crude and NGL segment. Long-duration interest rate levels are a structural headwind for pipeline infrastructure businesses, which carry significant debt loads: Enbridge plans approximately C$10 billion in debt issuance in 2026, though management has hedged a meaningful portion of the rate exposure. Investors should also monitor the pace of energy transition policy — though Enbridge's diversification across liquids, gas, utilities, and renewables provides meaningful insulation against single-scenario policy shocks.

ENB Scorecard

| Metric | Data |

|---|---|

| Current Price | ~US$48 (NYSE) |

| Market Cap | ~US$105 billion |

| Annual Dividend (USD) | ~$2.69/share (~5.6% yield) |

| FY2026 EBITDA Guidance | C$20.2B–C$20.8B |

| DCF/Share Guidance | C$5.70–C$6.10 |

| Citi Price Target | US$77 |

| Secured Growth Backlog | C$39 billion (+35% YoY) |

| Consecutive Dividend Growth | 31 years |

The Unified Frame: Three Picks, One Thesis

Materion, Johnson Controls, and Enbridge belong to entirely different industries. They share one investment logic: all three supply the prerequisite infrastructure that AI computing cannot function without. GPUs require precision materials to be manufactured. Once running, they require industrial-grade thermal removal to continue operating. And the facilities housing them require firm power delivered through gas pipelines. This sequence is not going away. It is, if anything, accelerating — as AI cluster sizes grow from tens of thousands of GPUs to hundreds of thousands, demand for all three categories of infrastructure compounds at the same rate.

What makes this trio particularly interesting as a portfolio combination is that their risk profiles and return characteristics are genuinely complementary. Materion offers growth optionality with semiconductor cycle exposure and defense durability. Johnson Controls offers a visible earnings ramp with a record backlog and Nvidia-backed data center positioning — the highest near-term momentum of the three. Enbridge offers the portfolio's defensive income layer: a 5.6% yield, 31 years of uninterrupted dividend growth, and contracted infrastructure cash flows that are structurally disconnected from short-term market sentiment. Together, they provide AI infrastructure exposure without concentration in any single sector, with three distinct risk-reward profiles that balance each other across the portfolio. While the market's attention remains fixed on the obvious names in the AI trade, Materion is refining the alloys, Johnson Controls is cooling the servers, and Enbridge is delivering the gas. The infrastructure buildout does not pause while investors debate valuations. It simply continues — and these three companies continue to get paid for it.

This article is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. All investment decisions should be made based on your own research, financial situation, and risk tolerance. Past performance does not guarantee future results.