The Won Is the Warning: Why KRW/USD Volatility Is the Real Risk Hiding Inside the KOSPI Rally

The KOSPI surged 75% in 2025 and broke 6,000 for the first time in history. But underneath the celebration, South Korea faces a convergence of dollar-denominated financial obligations — defense payments, investment pledges, and tariff-driven export compression — that could keep the Korean won structurally weak and equity markets structurally fragile through 2026.

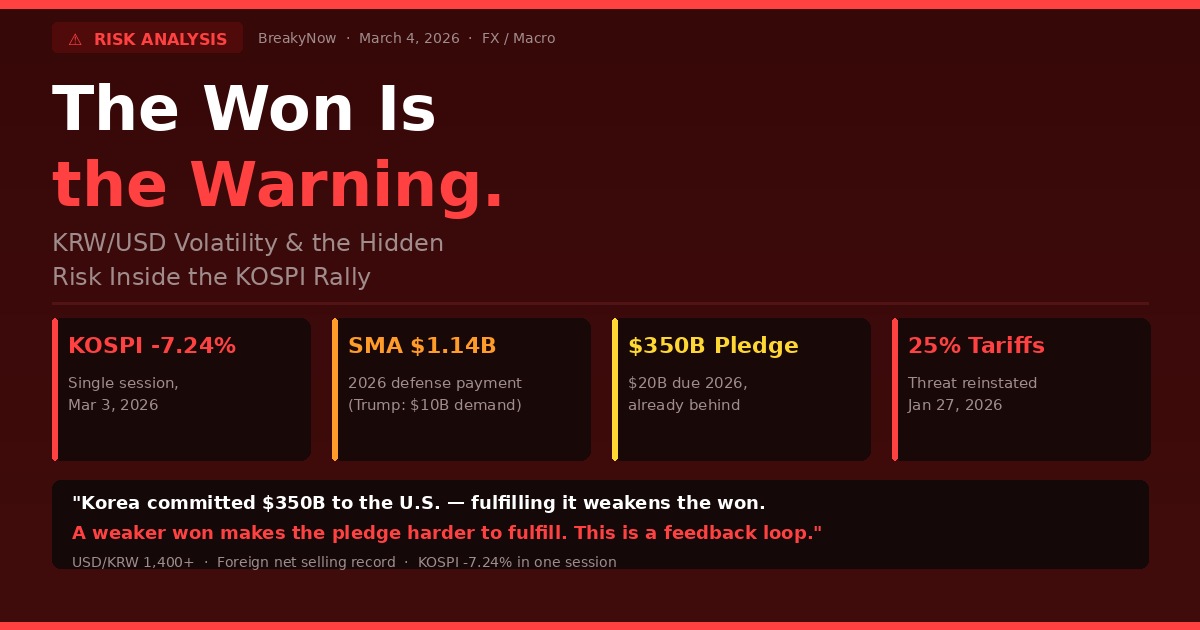

On the surface, South Korea's equity market story in 2025 and early 2026 looked like a redemption arc. A market derided for years as a structural laggard, plagued by the so-called "Korea Discount," delivered a 75.6% annual return, drove the KOSPI past the psychologically critical 6,000 threshold, and prompted brokerages to project 5,000 and then 6,000 as base cases for a market that had spent years failing to hold 3,000. The structural reform narrative — improved corporate governance, cancelled treasury shares, the "Value-Up" initiative, a new government committed to shareholder returns — gave the rally intellectual credibility that purely momentum-driven moves usually lack. But financial markets have a habit of exposing the weakest structural link at precisely the moment when confidence is highest. For South Korea in 2026, that link is the Korean won. On March 3, 2026, the KOSPI fell 7.24% in a single session, erasing weeks of gains as the won weakened simultaneously, compounding foreign outflows and adding to imported inflation pressures. That single day offered a preview of what a sustained KRW/USD deterioration could mean for the equity market beneath it.

The KOSPI's Achilles Heel: Everything Is Denominated in Won, But Everything That Matters Is Priced in Dollars

Understanding why KRW/USD is the critical variable for the KOSPI requires understanding the architecture of South Korea's economy. Korea is one of the most trade-dependent economies in the developed world — trade accounts for approximately 85% of GDP. Its largest companies, Samsung Electronics, SK Hynix, Hyundai Motor, Kia, LG Energy Solution, are overwhelmingly export-driven, generating revenue primarily in U.S. dollars while incurring a significant portion of costs in Korean won. In a falling-won environment, a surface-level analysis would suggest this is positive: dollar revenues converted back to won produce more won-denominated earnings, which supports stock prices. And this was the bull case that many investors cited when the won weakened through 2024 and 2025 — KRW weakness is a tailwind for exporters.

That analysis is correct in isolation and dangerously incomplete in practice. A weak won environment carries multiple simultaneous counterforces that offset the earnings tailwind. First, South Korea is a massive net energy importer. Oil, gas, and raw materials are priced in dollars. When the won falls, the cost of powering every factory and heating every building in the country rises in won terms — creating persistent domestic inflation that the Bank of Korea must address through interest rate policy, which in turn raises the cost of capital for the businesses whose earnings are supposedly being helped by the weak currency. Second, foreign investors — who hold a substantial portion of KOSPI free float — calculate their returns in dollars. When the won falls, a KOSPI stock that rises 10% in KRW terms can simultaneously produce a negative return in USD terms. This creates a structural incentive for foreign capital to exit Korean equities during periods of won depreciation, regardless of what the underlying businesses are doing. In February 2026, overseas investors posted record net equity sales on the KOSPI. The won's weakness was the direct catalyst. Third, the Bank of Korea's intervention — both verbal and through mechanisms like the National Pension Service's strategic hedging program — creates volatility of its own. Every time the government signals concern about "excessive" KRW weakness, the market interprets it as confirmation that the weakness is structural rather than transient, which tends to accelerate the very outflows the intervention was designed to prevent.

The Dollar Drain: What South Korea Actually Owes the United States in 2026

The deeper problem for the KRW in 2026 is not the cyclical sensitivity of the currency to U.S. interest rates or global risk appetite. It is a set of specific, quantified, dollar-denominated obligations that the South Korean government has committed to fulfilling — and that require either direct dollar outflows from Korea's reserves or the conversion of won into dollars at scale, both of which exert structural downward pressure on the KRW.

Layer 1: The Special Measures Agreement — The Baseline Obligation

South Korea's defense cost-sharing obligation to the United States is governed by the Special Measures Agreement (SMA), a framework first established in 1991 that requires Seoul to partially fund the stationing of approximately 28,500 U.S. troops in the country. The 12th SMA, signed in November 2024 and covering the period 2026–2030, sets South Korea's 2026 contribution at 1.52 trillion won ($1.14 billion) — an 8.3% increase over the 2025 level of 1.4 trillion won. The deal caps future annual increases at 5% and ties growth to the Korean Consumer Price Index. On its own terms, this is a manageable obligation. But it exists within a broader negotiating environment that has fundamentally changed since the agreement was signed.

Layer 2: Trump's $10 Billion Demand — The Renegotiation Shadow

The 12th SMA was signed specifically to lock in a favorable deal before Donald Trump's potential return to the presidency. The urgency was justified. Within months of Trump's inauguration for a second term, he publicly stated that South Korea should be paying $10 billion per year for the USFK presence — nearly nine times the current level — describing South Korea as a "money machine" and questioning why the U.S. was providing military protection "for essentially very little." Trump's first-term negotiating posture, which included an initial demand of $4.7–$5 billion annually before eventually arriving at the current levels, established the pattern: open with an extreme number, create maximum pressure, accept a compromise that still represents a large increase. The 12th SMA was supposed to insulate Korea from this dynamic through 2030. But the Trump administration has shown no particular respect for agreements it did not personally negotiate, and the combination of tariff threats and public statements about Korea's "insufficient" payments creates a persistent cloud of renegotiation risk over the current SMA framework.

Layer 3: The $350 Billion Investment Pledge — The Dollar Commitment That Is Already Behind Schedule

The most significant and least discussed dollar-denominated obligation is South Korea's commitment to invest $350 billion in the United States as part of the trade framework reached between the two countries in 2025. The Trump administration explicitly offered tariff relief — reducing South Korea's country-specific IEEPA tariff from 25% to 15% — in exchange for this investment pledge. The agreement requires $20 billion of investment in 2026 alone as the first tranche. South Korea has already fallen behind. A Bloomberg report in January 2026 suggested that Korea would not fulfill the $20 billion 2026 pledge on schedule, citing concerns over the continuing weakness of the KRW — the irony being that fulfilling the pledge requires converting won into dollars and sending those dollars to the U.S., which itself weakens the won, which makes the pledge harder to fulfill. South Korean Finance Minister Koo Yun-cheol acknowledged that investment in the first half of 2026 was "unlikely," even while insisting that the commitment remains intact. Trump's response was to announce a tariff increase to 25% on January 27, 2026, directly citing the legislative and investment delays. The confrontation establishes a feedback loop: delay in fulfilling dollar-denominated investment obligations → U.S. tariff threats → KRW depreciation on Korean export risk → further difficulty in fulfilling dollar obligations → additional U.S. pressure.

Layer 4: The 25% Tariff Threat — The Export Revenue Squeeze

Compounding the direct dollar obligation pressure is the impact of tariffs on Korea's dollar earnings capacity. In 2024, the U.S. trade deficit with South Korea was approximately $66 billion — the ninth-largest U.S. bilateral deficit. The U.S. has imposed, or threatened to impose, a cascade of sector-specific tariff actions on Korean exports: 25% automobile tariffs under Section 232, 50% steel and aluminum tariffs, ongoing investigations into semiconductors and pharmaceuticals, and the recurring reciprocal tariff threats that have oscillated between 10%, 15%, and 25% over the past year. Each tariff escalation reduces Korean exporters' dollar revenues — the same revenues that, when repatriated to Korea, support the won's value. Semiconductor exports are the most critical variable. Samsung Electronics and SK Hynix together represent 52% of KOSPI's projected 2026 net profits and 68% of the profit increase. Any material compression in semiconductor export earnings — whether through tariffs, demand slowdown, or supply chain disruption — directly impairs the KOSPI's earnings base while simultaneously removing a critical source of dollar inflows that support the won.

The KRW/USD Transmission Mechanism: How Currency Weakness Becomes Stock Market Risk

The relationship between KRW/USD and the KOSPI is not linear, and it is not always negative — but the conditions under which it becomes severely negative are now present simultaneously for the first time in years. Here is the specific transmission mechanism that investors should understand.

When the won weakens because of genuine export competitiveness — when Korean companies are winning global market share, generating more dollars, and the won's depreciation reflects the conversion of surplus dollars back into won — the stock market can rally alongside a weaker currency. This was roughly the dynamic in 2024 and parts of 2025. But when the won weakens because of capital outflows, policy uncertainty, and external financial pressure — as is increasingly the case in 2026 — the relationship inverts. Foreign investors hold roughly 30% of KOSPI free float. Their cost basis is in dollars. When the won falls 10%, they need the KOSPI to rise 10% in won terms just to break even in their own currency. If the KOSPI merely holds flat or rises modestly, they are losing money in dollar terms, and the rational response is to reduce Korea exposure. This foreign selling creates additional won supply, which pushes the exchange rate higher (more won per dollar), which makes the returns look even worse in dollar terms, which triggers more selling — a self-reinforcing cycle that in its most acute form is what currency crises look like.

The March 3, 2026 selloff provided a precise illustration of this mechanism in motion. The KOSPI fell 7.24% as the won depreciated simultaneously. Samsung Electronics fell 9.88%, SK Hynix fell 11.50%, Hyundai Motor fell 11.72%, and Kia Corp fell 11.29% — the exact same companies whose earnings are supposedly being helped by won weakness. Foreign investors posted near-record net sales. The won's weakness didn't protect those stocks; it accelerated their decline by triggering dollar-denominated investors to exit.

The Bank of Korea's Difficult Position

South Korea's central bank finds itself in a structurally constrained position that limits its ability to defend the won without creating new problems. The Bank of Korea has been cutting interest rates to support a sluggish domestic economy, but rate cuts reduce the interest rate differential between Korean and U.S. assets, making KRW-denominated investments less attractive relative to dollar-denominated ones and adding to won depreciation pressure. Raising rates to defend the currency would risk deepening domestic economic weakness, particularly in the heavily indebted household sector and the real estate market. The government has attempted to address this through the National Pension Service's strategic hedging program — the NPS manages nearly US$600 billion in foreign assets, and even marginal changes in its hedging ratio can produce large-scale dollar selling that supports the won. But as Bank of America noted, Korean retail investors purchased US$51 billion in net foreign securities in 2025 — a scale of dollar demand that the NPS hedging program is not designed to fully offset. The structural outflow of Korean household savings into U.S. and global equities represents a persistent, long-duration demand for dollars that is structurally bearish for the won regardless of central bank policy.

The Scenario Map: How Much Further Can USD/KRW Rise?

Against this backdrop, the question investors must answer is not whether KRW volatility will persist — it will — but how far the exchange rate could move under different scenarios, and what that means for Korean equity returns. ING's December 2025 forecast called for USD/KRW to appreciate from current levels to 1,375 by mid-2026 before returning to 1,400 by year-end — a relatively benign outcome predicated on Fed rate cuts, an end to the Bank of Korea's easing cycle, and easing trade tensions. That forecast was written before the January 2026 tariff escalation, before the investment pledge delays became public, and before the March 2026 geopolitical shock pushed the KOSPI down 7% in a single session.

A more stress-tested scenario analysis suggests meaningfully wider ranges. If the Trump administration follows through on 25% tariffs across all Korean export categories — a plausible outcome given the legislative and investment delays — Korean export revenues face a material shock that would reduce dollar inflows, pressure the KRW, and compress the earnings of KOSPI's most heavily weighted companies simultaneously. If the SMA renegotiation produces a significantly higher defense payment — even half of Trump's stated $10 billion target would represent a 4x increase — the dollar outflow requirement would dwarf anything Korea has budgeted for and would require either drawing down foreign exchange reserves or direct won-to-dollar conversion at scale. The worst-case compound scenario — tariff escalation plus SMA renegotiation plus investment pledge shortfall plus ongoing retail dollar demand — could plausibly push USD/KRW toward 1,500 or beyond. At those levels, the KOSPI's apparent cheapness in won terms would be largely or entirely offset by exchange rate losses for the dollar-based investor base that needs to remain engaged for Korean equities to sustain their current valuation levels.

The Investor Framework: What to Watch

This analysis does not argue that the KOSPI's structural reform story is wrong or that Korean equities are uninvestable. The governance improvements are real. The semiconductor cycle is real. The earnings growth trajectory is real. What it argues is that those fundamental strengths exist within a currency framework that is under simultaneous pressure from multiple directions, and that KRW/USD is the variable that most determines whether international capital can stay long Korean equities long enough to realize the fundamental value that domestic analysts correctly identify. For investors monitoring this situation, the critical variables to track are: the pace and scale of South Korea's $20 billion 2026 U.S. investment pledge fulfillment; any official statement from the Trump administration regarding SMA renegotiation; the USD/KRW level relative to the Bank of Korea's intervention thresholds; the pace of foreign net selling on the KOSPI; and the semiconductor export data released every 10 days by the Korean Customs Service, which is the single best leading indicator for both corporate earnings and won stability.

South Korea's equity market spent years being dismissed as uninvestable. The 2025 rally forced a reassessment. But markets that are re-rated quickly on structural grounds are also markets where the structural thesis gets tested most harshly when a new risk emerges. The won is the test. And the test is already underway.

This article is for informational purposes only and does not constitute financial or investment advice. All investment decisions should be based on independent research and individual risk tolerance. Exchange rates and equity market conditions are subject to rapid change.