AAOI: The Hidden $300 Stock Nobody Is Watching — Until Now

Applied Optoelectronics surged over 55% in a single session on February 27, 2026. It has risen more than 750% from its 52-week low. And the real move hasn't even started yet.

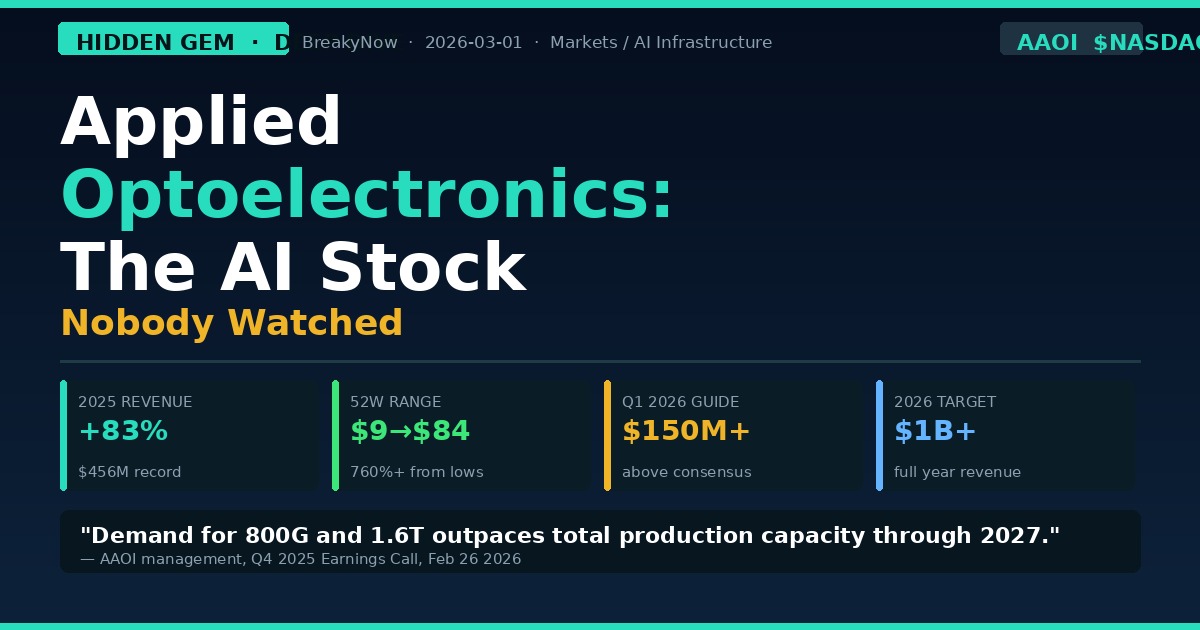

There is a category of stock that becomes visible only in hindsight — the company that was doing the right work, in the right place, at exactly the right moment in history, while the market's attention was fixed on flashier names nearby. Applied Optoelectronics, Inc. (NASDAQ: AAOI) has spent the past eighteen months becoming one of the most compelling examples of this phenomenon in the AI infrastructure buildout. While investors poured hundreds of billions into Nvidia, Palantir, and the hyperscalers themselves, almost nobody talked about the $5 billion company in Sugar Land, Texas that manufactures the fiber-optic transceivers that physically connect those GPUs to each other. On February 27, 2026, the stock rose more than 55% in a single trading session, reaching an 8-year high. It has climbed from a 52-week low of $9.71 to an intraday high of $84.31. And according to management's own guidance, the company's most important growth catalyst — the mass production ramp of its 800G and 1.6T generation transceivers — has not yet fully materialized. The run may be just beginning.

🔬 What Applied Optoelectronics Actually Does

Applied Optoelectronics was founded by Dr. Thompson Lin in 1997 with a singular focus: design and manufacture every critical component in a fiber-optic transceiver in-house, rather than assembling parts from third-party suppliers. The company operates what the industry calls a vertically integrated manufacturing model — meaning it grows its own semiconductor laser chips from raw materials using proprietary Molecular Beam Epitaxy (MBE) reactors, packages them into optical components, assembles those components into transceivers, and ships the finished modules to data center operators. This is an extraordinarily rare capability in the optics industry. Most transceiver companies are assemblers — they buy laser chips from one vendor, optical filters from another, and put them together. AAOI grows the lasers itself. This gives the company three structural advantages that are only now being appreciated at scale: cost control at the component level, supply chain independence, and the ability to customize optical performance specifications that pure assemblers cannot match.

The company's business divides into two distinct segments. The first is its legacy Cable TV (CATV) business, which supplies optical amplifiers, headend equipment, and HFC (Hybrid Fiber-Coaxial) networking components to cable operators including Charter Communications — one of the largest cable providers in the United States. This segment has provided a steady revenue base for years and is now experiencing its own upgrade cycle as cable operators deploy DOCSIS 4.0 infrastructure. The second and far more exciting segment is its data center transceiver business, where AAOI manufactures the 400G, 800G, and emerging 1.6T optical transceivers that hyperscale cloud operators — Amazon, Microsoft, Meta, Oracle, and others — require to connect their AI compute clusters. Every cluster of GPU servers in a modern AI data center requires thousands of high-speed optical connections. At the scale of clusters containing hundreds of thousands of H100 or B200 Nvidia GPUs, those connections must operate at speeds that copper interconnects physically cannot achieve. Optical transceivers are not optional. They are as fundamental to AI infrastructure as the chips themselves — and they are AAOI's core product.

📊 The 2025 That Changed Everything: Revenue Up 83% Year-Over-Year

The 2025 fiscal year marked a fundamental transformation for Applied Optoelectronics that most of the financial media entirely missed. Total revenue reached a record $455.72 million, representing an 82.75% increase over 2024's $249.37 million. Losses, while still present, shrank by 79.5% year-over-year as gross margins expanded rapidly, reaching 29.3% in Q4 — more than 10 percentage points above the year-ago level.

The quarterly progression tells an even more dramatic story. Q1 2025 revenue came in at $99.9 million — up 145% year-over-year. Q3 2025 hit $118.6 million, nearly doubling year-over-year. Q4 2025, reported on February 26, 2026, delivered $134.27 million, up 33.9% from the same period a year earlier and slightly above the $131.56 million analyst consensus. But the more significant number from the Q4 report was not the revenue — it was the adjusted EPS of -$0.01, compared to the consensus expectation of -$0.12. The company came within a single penny of breaking even for the quarter, a feat that management guided was achievable as recently as mid-2025 but that most analysts had written off as optimistic. The stock's reaction — a 55% single-session surge — reflected not just the Q4 result, but the recalibration of the entire forward earnings model.

CEO Dr. Thompson Lin's statement on the earnings call captured the moment: "Total revenue increased 83% compared to 2024 to a record $456 million." He cited "robust demand in both our CATV and data center business" and confirmed the company received its fourth major 800G volume order from a hyperscale customer — with full production ramp expected after firmware qualification completion in March 2026.

🚀 The 800G Supercycle: Why This Is Only the Beginning

The single most important fact about Applied Optoelectronics in 2026 is not where it has been — it is where the market is going. TrendForce projects that global shipments of 800G-and-above transceivers will leap from approximately 24 million units in 2025 to nearly 63 million units in 2026 — a 2.6x increase in a single year. The driver is straightforward: as AI data centers scale from clusters of tens of thousands of GPUs to clusters of hundreds of thousands, the bandwidth requirements between compute nodes are growing faster than any previous technology transition in the industry. Traditional 400G transceivers, which have been the workhouse of hyperscale data centers for the past several years, are becoming bottlenecks. The industry is in the midst of an accelerated migration to 800G, with 1.6T beginning qualification cycles simultaneously.

AAOI is positioned directly at the center of this transition. The company has now received four separate volume orders for 800G transceivers from hyperscale customers. Its production capacity has ramped from approximately 10,000–20,000 units per month at the start of 2025 to roughly 90,000 units per month by year-end 2025. Management confirmed in the Q4 2026 earnings call that capacity is targeting more than 200,000 units per month by mid-2026, with approximately 40% of that production occurring at the new Sugar Land, Texas facility — a strategic alignment with hyperscalers' growing preference for U.S.-manufactured components in the context of trade policy uncertainty. Most critically, management stated explicitly on the call that demand for 800G and 1.6T products currently exceeds total production capacity through mid-2027. AAOI is not chasing customers. It is racing to build enough manufacturing to fill orders it already has.

The Amazon relationship deserves particular attention. AAOI has secured a reported $4 billion, 10-year purchase agreement with Amazon Web Services — a contract that provides extraordinary revenue visibility and de-risks the capital expenditure program required to fund the production ramp. B. Riley's February 27 upgrade noted that "demand remains robust, led by steady order flow from key customer Amazon," while confirming that 800G transceivers are expected to be a primary growth driver beginning in Q2 2026. The Needham upgrade to a $80 price target on the same day echoed the same thesis, calling the company's trajectory a potential "10x moment."

🏭 The Texas Bet: $300 Million in Domestic Manufacturing

On the same day as its Q4 earnings release, Applied Optoelectronics held a groundbreaking ceremony for a new 210,000 square-foot manufacturing facility in Sugar Land, Texas — and announced it was doubling the planned investment from $150 million to $300 million, with a commitment to create up to 500 new jobs. This is not a symbolic gesture. It is a strategic repositioning designed to capture a specific procurement preference that has emerged among hyperscale customers in the post-tariff-era trade environment.

As the Trump administration's tariff policies — including Section 232 measures and IEEPA-based country-specific tariffs — continue to reshape global supply chains, hyperscalers are under both regulatory and reputational pressure to source critical AI infrastructure components from domestic or allied manufacturers. AAOI's existing Taiwan facility provides supply chain diversification outside of China, while the new Texas facility positions the company as the only transceiver manufacturer with significant vertically integrated production capacity in the continental United States. When major cloud operators are spending $50 billion to $100 billion annually on AI infrastructure and facing congressional scrutiny over supply chain dependencies, having a U.S. supplier capable of producing 800G transceivers at scale is not a minor advantage. It is a procurement checkbox that AAOI alone can tick.

💰 The Numbers: From Survival Mode to $1 Billion in Revenue

The guidance issued alongside Q4 2025 results is, by any measure, extraordinary for a company that was trading below $10 per share just over a year ago. For Q1 2026, management guided revenue of $150 million to $165 million — above the $145.6 million analyst consensus — with gross margins expected to hold in the 29%–31% range as product mix shifts toward higher-margin 800G products. More significantly, management stated on the earnings call that the company is targeting over $1 billion in full-year 2026 revenue, implying continued sequential growth at a pace that would make AAOI one of the fastest-scaling companies in the semiconductor supply chain.

The path to profitability is now visible in the numbers. The aggressive capital expenditure program — $209 million in 2025 — is expected to continue at elevated levels in 2026 as new manufacturing lines come online. But the gross margin trajectory, moving from 18.7% in Q1 2025 to 29.3% in Q4 2025, suggests that automation and vertical integration are delivering the operating leverage that the bull thesis always depended on. Management projected, in a previous guidance framework, achieving over $150 million in net profit for 2026 — a figure that, if achieved, would represent a profitability inflection that rewrites the entire valuation framework for the stock. The company also entered into an equity distribution agreement with Raymond James and Needham & Company to raise up to $250 million through at-the-market share sales — dilutive on the surface, but reflecting confidence in the company's ability to deploy that capital productively into the capacity expansion.

⚠️ The Risks That Are Also Real

The AAOI thesis is compelling, but it comes with a risk profile that demands honest accounting. The company carries a beta of 3.32 — meaning it moves roughly three times as much as the broader market in either direction. Its stock has spent most of the past decade below $20, and the current run reflects a combination of fundamental improvement and narrative momentum that can reverse sharply if execution stumbles. The key risks to monitor are specific and well-defined.

Customer concentration is the most immediate concern. A substantial portion of AAOI's data center revenue comes from a small number of hyperscale customers, with one major hyperscale customer accounting for nearly $22 million in 400G orders in 2025 alone. Any slowdown in hyperscale AI capex — whether driven by macroeconomic conditions, a reset in AI investment sentiment, or customer-specific budget shifts — would hit AAOI disproportionately. The firm itself notes that supply chain and manufacturing execution, not market demand, is currently the binding constraint — but that constraint, while flattering for the near-term revenue narrative, also means the company is deeply dependent on its ability to execute an extremely demanding manufacturing ramp on schedule. The firmware qualification for 800G transceivers, expected to complete by mid-March 2026, is a near-term binary event: successful completion unlocks a major production ramp in Q2; any delay reprices the quarter. Competition from larger players — Lumentum, Coherent, and Ciena — all of which have deeper balance sheets and established hyperscale relationships — remains a structural ceiling on AAOI's long-term pricing power. And the ongoing dilution from equity issuances, which has nearly doubled the share count over the past two years, is a headwind that will limit per-share earnings growth even as absolute profits improve.

The Thesis in Plain English

Strip away the jargon, and the Applied Optoelectronics story is the simplest kind of investment thesis: a company that makes something that every AI data center in the world must have, that is the only vertically integrated domestic manufacturer of that thing, that has just won multi-year contracts with the largest buyers of that thing, and that is racing to build the production capacity to fill orders it already possesses. The $456 million 2025 revenue and the guidance for $1 billion+ in 2026 are not projections built on speculation. They are the math of orders already placed, facilities under active construction, and production lines already running. The 52-week low of $9.71 reflects where the market was before that math became undeniable. The 55% single-session surge on February 27 is the market catching up to what the order books have been saying for months.

AAOI is not a meme stock. It is not an AI narrative play with no revenue. It is a manufacturing company with $456 million in trailing twelve-month sales, a $4 billion contract with Amazon, a new factory in Texas, and guidance for $1 billion in revenue before the year is over. For investors who believe that the AI data center buildout has years of runway remaining — and that the physical infrastructure connecting those data centers requires the same uninterrupted supply of optical components that electricity generation requires turbines — Applied Optoelectronics is the stock that the market somehow forgot to tell anyone about.

Now the market is remembering.

This article is for informational purposes only and does not constitute financial advice. AAOI carries a beta of 3.32 and significant volatility risk. Always conduct thorough due diligence before making any investment decisions. Past stock performance does not guarantee future results.